To close the significant global infrastructure investment gap, we need to know how much is currently being invested in infrastructure – by both the public and private sectors.

Unfortunately, there is a global and longstanding lack of consolidated, consistent, and current data on infrastructure investment levels and trends. In the absence of such data, Gross Fixed Capital Formation (GFCF)[1] for General Government is often used as a proxy for public infrastructure investment, despite its significant issues.

The GI Hub’s InfraTracker aims to help address this data gap by analysing public investment data presented in G20 government budgets. It is the first tool of its kind and scale to be developed with the cooperation of G20 governments and is a new and very reasonable proxy for gauging trends in public investment in infrastructure.[2]

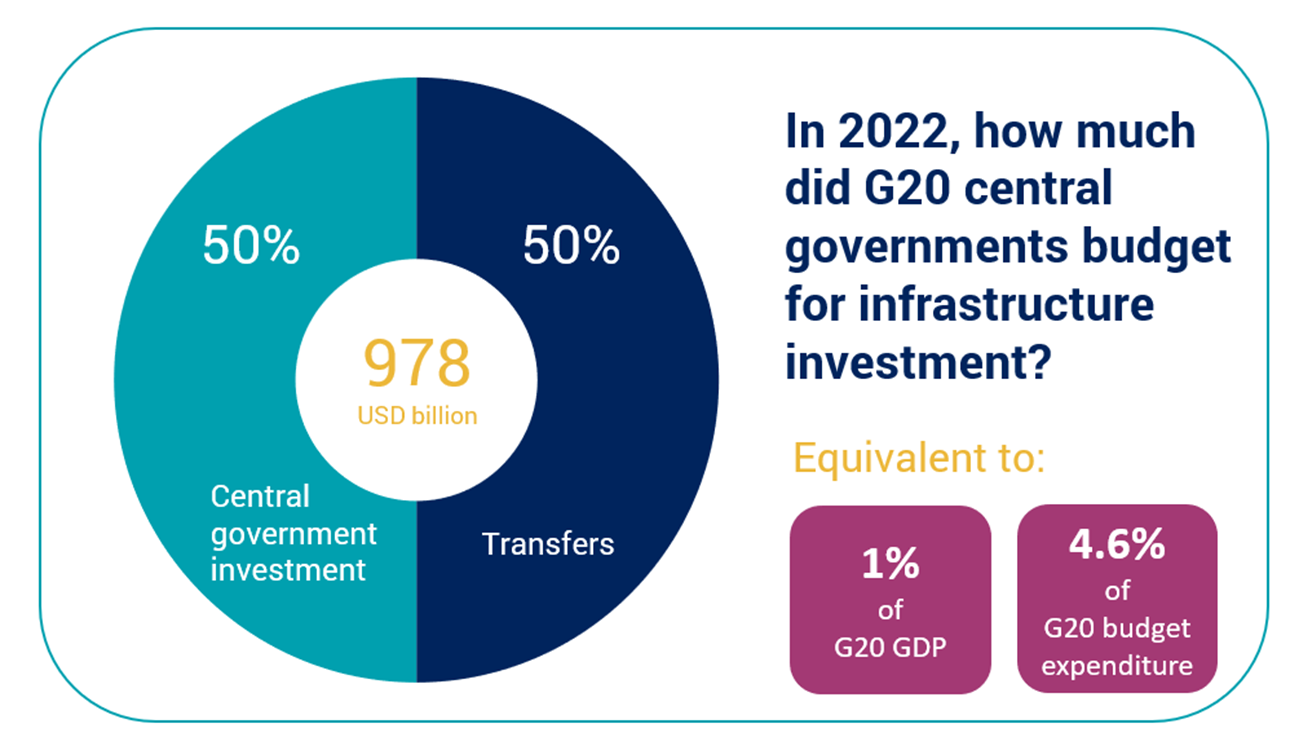

InfraTracker estimates that G20 central governments budgeted almost USD1 trillion for infrastructure investment in 2022, equivalent to around 1% of total G20 GDP or 4.6% of total G20 central government budget expenditure. Of this, 50% was central governments investing directly into infrastructure, and 50% was transfers to other levels of government for investment in infrastructure.

71% of the USD1 trillion is in advanced G20 economies and 29% in emerging G20 economies. This trend is mirrored in private sector investment; our Infrastructure Monitor shows that 80% of private investment in infrastructure projects occurred in high-income countries in 2021, and only 20% in middle- and low-income countries.

The USD1 trillion represents a small share of the annual global infrastructure investment needed to keep pace with economic growth and achieve global climate goals and the UN Sustainable Development Goals (SDGs). For example, McKinsey estimates that USD 3.7 trillion is needed annually to keep pace with projected GDP growth and up to a further USD1 trillion to meet the SDGs. These are also underestimates as they only include economic, and not social (such as health, education, or housing), infrastructure needs. Meanwhile, the IEA estimates that total annual capital investment in energy must reach almost USD5 trillion by 2030 in order to achieve net zero by 2050.

Although levels of public investment in infrastructure are significantly higher than levels of private investment (particularly in developing economies where public investment has been reported to represent around 83% of investment), governments are facing challenges due to fiscal constraints. Unprecedented fiscal spending in response to the COVID-19 pandemic saw public debt levels reach 100% of GDP in 2020, a record high (IMF, 2022). Debt levels have since declined due to strong growth and higher inflation, but they remain elevated and well above pre-pandemic levels. To meet growing global infrastructure needs, it is essential to scale up private capital for infrastructure.

{kind=link}